Volatility and uncertainty are not the same!

Crude oil price volatility is often viewed as reflecting uncertainty not only related to the oil market, but also to the global macroeconomic environment. However, the question arises as to whether uncertainty is not likely to be at play without generating high volatility on the oil market.

Par Valérie Mignon, Marc Joëts, Tovonony Razafindrabe

The influence of macroeconomic uncertainty on oil price fluctuations has not been widely addressed though this question is of particular interest given the modern view that the price of oil is mainly endogenous with respect to global macroeconomic conditions.

Measuring macroeconomic uncertainty

Examining the impact of uncertainty on market dynamics is a challenging question for economists because no objective measure of uncertainty exists. Although in a general sense uncertainty is defined as the volatility of an unforecastable disturbance, the empirical literature to date has usually relied on proxies. The most common measures used are the implied or realized volatility of stock market returns, the cross-sectional dispersion of firm profits, stock returns, or productivity, and the cross-sectional dispersion of survey-based forecasts. However, their adequacy to correctly proxy uncertainty is questionable, and such measures are even misspecified with regard to the theoretical notion of uncertainty. Indeed, stock market volatility, cross-sectional dispersion in stock returns and firm profits can vary over time due to several factors—such as risk aversion, the leverage effect, and heterogeneity between firms—even if there is no significant change in uncertainty. In other words, fluctuations that are actually predictable can be erroneously attributed to uncertainty, putting forward the importance of distinguishing between uncertainty in a series and its volatility. Specifically, in a recent CEPII Working Paper aiming at investigating the link between commodity price volatility and macroeconomic uncertainty, we consider a consistent measure of macroeconomic uncertainty by linking uncertainty to predictability.[1] This measure uses a wide range of monthly macroeconomic and financial indicators: it is indeed defined as the common variation in uncertainty across around 280 series rather than uncertainty related to any single series. This is in line with the uncertainty-based business cycle theories which implicitly assume a common variation in uncertainty across a large number of series.

Transmission of macroeconomic uncertainty to oil market uncertainty

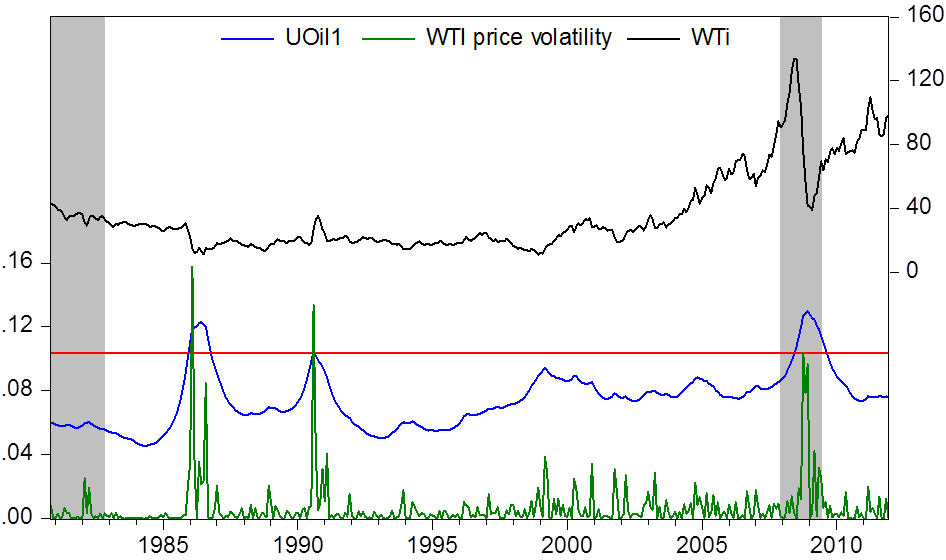

Figure 1 displays the evolution of uncertainty in the oil market (blue line), together with the evolution of corresponding prices (black line) and volatility (green line). When uncertainty in the oil market exceeds the horizontal red bar, this refers to episodes of heightened uncertainty for the oil price return series. When oil price uncertainty coincides with the vertical gray bands—representing macroeconomic uncertainty periods—it indicates a potential transfer from macroeconomic to oil market uncertainty (with both uncertainty episodes occurring in the same period).[2] Otherwise, uncertainty is attributable to the own characteristics of the oil market.

As shown, the sensitivity of oil price uncertainty to macroeconomic uncertainty differs depending on the period considered, highlighting that oil shocks do not all follow the same pattern. For example, the period that just follows the invasion of Kuwait in 1990 or, to a lesser extent, the Iraq war in 2002-03 are episodes characterized by sharp spikes in oil prices. The Iran-Iraq war starting at the beginning of the 1980s is, in contrast, associated with small price movements. As stressed by Barsky and Kilian (2004), a simplistic view should be that major war episodes cause price uncertainty to increase through a rise in precautionary demand for oil. However, among all episodes of important fluctuations in oil prices, only two seem to be accompanied by uncertainty: (i) the 2007-09 recession, and (ii) the 1984-86 period. During the 2007-09 recession, oil price uncertainty is indeed very sensitive to macroeconomic uncertainty, a result that can be linked to the well-known relationship that exists between economic activity and the oil market. This episode of high oil price uncertainty is accompanied by the biggest oil price spike in the postwar experience and results from various macroeconomic factors. Whatever the origin of price surges, this period of macroeconomic uncertainty is reflected in oil market uncertainty by an unprecedented oil price increase. The 1984-86 period is also characterized by heightened oil price uncertainty, but it does not coincide with macroeconomic uncertainty. This episode seems to be related to the conjunction of two events: (i) the production shutdown in Saudi Arabia between 1981 and 1985, which caused a strong price decrease; and to a lesser extent (ii) the OPEC collapse in 1986.

Overall, the recent 2007-09 recession generated an unprecedented episode of uncertainty in the price of oil. In addition, our analysis shows that macroeconomic uncertainty episodes are not necessarily accompanied by high volatility in the oil price. This major finding illustrates the interest of our measure of uncertainty, underlining that uncertainty is more related to predictability than to volatility. The relevance of the predictability-based approach could be explained by some specific properties of the oil market. In particular, this market is known to be characterized by a low elastic demand together with a strong inertial supply, making any unexpected adjustment difficult and costly. This importance of factors that are specific to the oil market is in line with the conclusions of the latest World Economic Outlook published by IMF (IMF, 2015) underlining that greater than expected oil supply and some weakness in the demand for oil linked to improvements in energy efficiency have played a key role in explaining the recent oil price collapse.

Marc Joëts is Economist at Ipag Lab and EconomiX-CNRS, University of Paris Ouest and Tovonony Razafindrabe is Economist at EconomiX-CNRS, University of Paris Ouest.

References:

Barsky, Robert B., and Lutz Kilian (2004), “Oil and the Macroeconomy since the 1970s”, Journal of Economic Perspectives 18(4), 115-134.

IMF (2015), World Economic Outlook, April.

Joëts Marc, Valérie Mignon and Tovonony Razafindrabe (2015), “Does the volatility of commodity prices reflect macroeconomic uncertainty?”, Working Paper CEPII 2015-02.

Measuring macroeconomic uncertainty

Examining the impact of uncertainty on market dynamics is a challenging question for economists because no objective measure of uncertainty exists. Although in a general sense uncertainty is defined as the volatility of an unforecastable disturbance, the empirical literature to date has usually relied on proxies. The most common measures used are the implied or realized volatility of stock market returns, the cross-sectional dispersion of firm profits, stock returns, or productivity, and the cross-sectional dispersion of survey-based forecasts. However, their adequacy to correctly proxy uncertainty is questionable, and such measures are even misspecified with regard to the theoretical notion of uncertainty. Indeed, stock market volatility, cross-sectional dispersion in stock returns and firm profits can vary over time due to several factors—such as risk aversion, the leverage effect, and heterogeneity between firms—even if there is no significant change in uncertainty. In other words, fluctuations that are actually predictable can be erroneously attributed to uncertainty, putting forward the importance of distinguishing between uncertainty in a series and its volatility. Specifically, in a recent CEPII Working Paper aiming at investigating the link between commodity price volatility and macroeconomic uncertainty, we consider a consistent measure of macroeconomic uncertainty by linking uncertainty to predictability.[1] This measure uses a wide range of monthly macroeconomic and financial indicators: it is indeed defined as the common variation in uncertainty across around 280 series rather than uncertainty related to any single series. This is in line with the uncertainty-based business cycle theories which implicitly assume a common variation in uncertainty across a large number of series.

Transmission of macroeconomic uncertainty to oil market uncertainty

Figure 1 displays the evolution of uncertainty in the oil market (blue line), together with the evolution of corresponding prices (black line) and volatility (green line). When uncertainty in the oil market exceeds the horizontal red bar, this refers to episodes of heightened uncertainty for the oil price return series. When oil price uncertainty coincides with the vertical gray bands—representing macroeconomic uncertainty periods—it indicates a potential transfer from macroeconomic to oil market uncertainty (with both uncertainty episodes occurring in the same period).[2] Otherwise, uncertainty is attributable to the own characteristics of the oil market.

|

Figure 1. Uncertainty and volatility in the oil market |

|

|

Note: This figure depicts the uncertainty proxy for the oil market (left axis, blue line). The horizontal red bar corresponds to 1.65 standard deviation above the mean of our oil-related uncertainty series (left axis). Vertical gray bands represent macroeconomic uncertainty periods. Volatility (green line) is proxied by the daily squared returns of prices (left axis). Black line refers to the price series (right axis).

|

As shown, the sensitivity of oil price uncertainty to macroeconomic uncertainty differs depending on the period considered, highlighting that oil shocks do not all follow the same pattern. For example, the period that just follows the invasion of Kuwait in 1990 or, to a lesser extent, the Iraq war in 2002-03 are episodes characterized by sharp spikes in oil prices. The Iran-Iraq war starting at the beginning of the 1980s is, in contrast, associated with small price movements. As stressed by Barsky and Kilian (2004), a simplistic view should be that major war episodes cause price uncertainty to increase through a rise in precautionary demand for oil. However, among all episodes of important fluctuations in oil prices, only two seem to be accompanied by uncertainty: (i) the 2007-09 recession, and (ii) the 1984-86 period. During the 2007-09 recession, oil price uncertainty is indeed very sensitive to macroeconomic uncertainty, a result that can be linked to the well-known relationship that exists between economic activity and the oil market. This episode of high oil price uncertainty is accompanied by the biggest oil price spike in the postwar experience and results from various macroeconomic factors. Whatever the origin of price surges, this period of macroeconomic uncertainty is reflected in oil market uncertainty by an unprecedented oil price increase. The 1984-86 period is also characterized by heightened oil price uncertainty, but it does not coincide with macroeconomic uncertainty. This episode seems to be related to the conjunction of two events: (i) the production shutdown in Saudi Arabia between 1981 and 1985, which caused a strong price decrease; and to a lesser extent (ii) the OPEC collapse in 1986.

Overall, the recent 2007-09 recession generated an unprecedented episode of uncertainty in the price of oil. In addition, our analysis shows that macroeconomic uncertainty episodes are not necessarily accompanied by high volatility in the oil price. This major finding illustrates the interest of our measure of uncertainty, underlining that uncertainty is more related to predictability than to volatility. The relevance of the predictability-based approach could be explained by some specific properties of the oil market. In particular, this market is known to be characterized by a low elastic demand together with a strong inertial supply, making any unexpected adjustment difficult and costly. This importance of factors that are specific to the oil market is in line with the conclusions of the latest World Economic Outlook published by IMF (IMF, 2015) underlining that greater than expected oil supply and some weakness in the demand for oil linked to improvements in energy efficiency have played a key role in explaining the recent oil price collapse.

Marc Joëts is Economist at Ipag Lab and EconomiX-CNRS, University of Paris Ouest and Tovonony Razafindrabe is Economist at EconomiX-CNRS, University of Paris Ouest.

References:

Barsky, Robert B., and Lutz Kilian (2004), “Oil and the Macroeconomy since the 1970s”, Journal of Economic Perspectives 18(4), 115-134.

IMF (2015), World Economic Outlook, April.

Joëts Marc, Valérie Mignon and Tovonony Razafindrabe (2015), “Does the volatility of commodity prices reflect macroeconomic uncertainty?”, Working Paper CEPII 2015-02.

[1] See Joëts et al. (2015).

[2] The gray bands correspond to episodes of important macroeconomic uncertainty: the months surrounding the 1973-74 and 1981-82 recessions and the 2007-09 great recession.

|

Retrouvez plus d'information sur le blog du CEPII. © CEPII, Reproduction strictement interdite. Le blog du CEPII, ISSN: 2270-2571 |

|||

|