Latin America : Investing in infrastructure is key to achieve long term sustained growth

The sharp drop in commodity prices has had a sizeable impact on Latin America's short term growth prospects. The decline in terms of trade has also revealed, once again, the low productivity of the region's economies. Investing in infrastructure could help Latin America simultaneously address these short and long term challenges.

Par Camilo Umana Dajud

The first decade of this century was for Latin America one of sustained growth, significant reductions in poverty rates and a constant widening of the middle class, all of which was accomplished while maintaining balanced fiscal policies. The economies of the region face nonetheless since the end of 2010 a number of renewed common challenges. Two of them are particularly relevant for the current and future economic performance of the region.

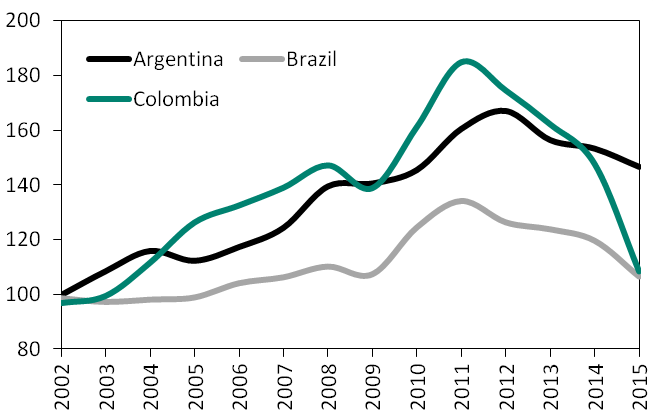

The first challenge the region is being confronted to is, not surprisingly, the drop in commodity prices. The sustained growth experienced by the region during the first decade of the 21st century was accompanied by a constant improvement of terms of trade (Figure 1). The beginning of the current decade coincided however with the start of a sharp decline in the price of most commodities produced and exported by the region. As shown by the graph below, Brazil and Colombia's terms of trade were in 2015 back to their 2004 levels. That is almost a 45% drop for Colombia and nearly 25% for Brazil.

The first challenge the region is being confronted to is, not surprisingly, the drop in commodity prices. The sustained growth experienced by the region during the first decade of the 21st century was accompanied by a constant improvement of terms of trade (Figure 1). The beginning of the current decade coincided however with the start of a sharp decline in the price of most commodities produced and exported by the region. As shown by the graph below, Brazil and Colombia's terms of trade were in 2015 back to their 2004 levels. That is almost a 45% drop for Colombia and nearly 25% for Brazil.

|

Figure 1 – Shared challenge #1: Terms of trade

|

|

|

Note: net barter terms of trade index 2000 = 100

Source: WDI, World Bank (2017). |

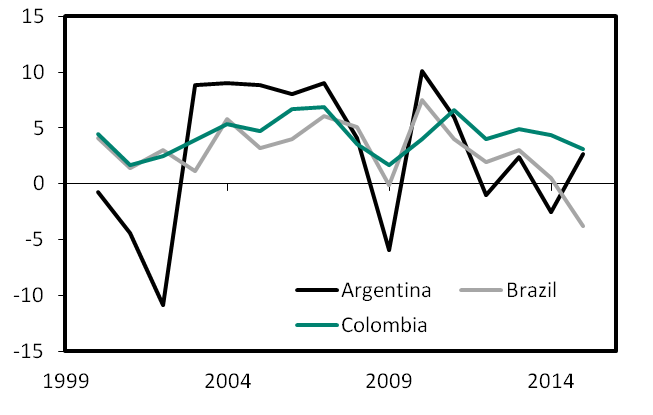

The steady decline in the region's terms of trade dragged economic growth. Argentina experienced a recession in 2014 followed by Brazil in 2015 (Figure 2). Colombia's growth is expected to drop from 6.6% in 2011 to 2.5% in 2017. In the short term the region needs therefore to address the drop in commodity prices. Sustaining the previously obtained gains in terms of the reduction in poverty rates and the rise of a wider middle class will depend on how this short term challenge is managed. The region has however long faced the fluctuation of raw materials and commodity prices. The improved terms of trade of the beginning of the century hid in fact, for a while, another common and long term challenge: the low productivity of Latin American economies.

|

Figure 2 – Annual real GDP growth rate (%)

|

|

|

Note: GDP growth rate

Source: WDI, World Bank (2017). |

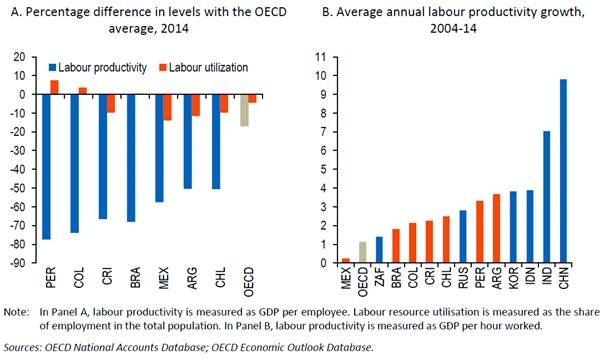

The graph below (Figure 3) summarizes two salient features of labor productivity in Latin America. First, productivity remains between 70% and 50% below the OECD average. Second, while productivity has grown in recent years above the OECD average, it has lagged behind the productivity growth of Asian emerging countries. Addressing this low productivity challenge is key for long term sustained growth and reducing the region's vulnerability to commodity price fluctuations.

|

Figure 3 – Shared challenge #2: Labor productivity

|

|

|

Source: OECD (2016), Promoting Productivity for Inclusive Growth in Latin America, OECD Publishing, Paris.

|

While these are shared challenges, the specific contexts of each economy in the region call for differentiated policy design and implementation. According to a number of international organizations simplifying the extremely complex tax system in Brazil should be a priority[1] , Colombia needs to improve access to pre-primary education[2] and Argentina must continue reducing the regulatory burden and trade barriers[3]. There is however one area that needs significant improvements in all the countries of the region: infrastructure[4]. Out of the 160 economies covered by the World Bank's Logistic Performance Index, Brazil ranks 55, Argentina 66, and Colombia only 94. Improved infrastructure is crucial to increase productivity and achieve long term sustained growth. Empirical studies show that infrastructure, by reducing domestic transport costs, has a permanent positive impact on income levels[5]. New or improved infrastructure reduces also the price of imported inputs and fosters exports and firms’ integration into global value chains. Moreover, the Keynesians effects of investment in infrastructure could also help the region face the short term negative growth impact of the deterioration of the terms of trade.

In the short term, the countries of the region must therefore address the effect of falling commodity prices. If this is not done they risk jeopardizing important social improvements obtained during the first decade of the century. In the medium and long term, the forward-looking agenda for this region needs to go much deeper: it must uncover a stronger and more sustainable growth trajectory by undertaking the comprehensive reforms needed to accelerate productivity growth.

[1] Arnold, J. (2016), “Raising Industrial Performance in Brazil”, OECD Economics Department Working Paper, forthcoming.

[2] http://www.oecd.org/eco/growth/Going-for-Growth-Colombia-2017.pdf

[3] IMF (2016), Argentina: 2016 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for Argentina, IMF Country Report No. 16/346.

[4] IDB (2015), Financing Infrastructure in Latin America and the Caribbean: How, How much and by Whom?.

[5] Banerjee, A., Duflo, E., & Qian, N. (2012). On the road: Access to transportation infrastructure and economic growth in China. Yale Department of Economics mimeo

|

Retrouvez plus d'information sur le blog du CEPII. © CEPII, Reproduction strictement interdite. Le blog du CEPII, ISSN: 2270-2571 |

|||

|