Covid-19 Crisis: Tracking uncertainty in the US economy

Updated from March 26 post.

The Covid-19 pandemic outbreak is continuing its rapid spread around the world. The fight against the pandemic is organized in a context of high uncertainty on the effectiveness of health policies.[1] Policy makers aim to prevent an explosion of financial and economic uncertainty and thereby to reduce the economic costs of the Covid-19 crisis.[2] The purpose of this blog is twofold. Firstly, it presents a dashboard to monitor the crisis by tracking uncertainty in the US economy. Daily indicators of stock market value, stock market volatility, credit spread and uncertainty on economic policy are being used to get a synthetic view of the current situation. Secondly, it aims at comparing the ongoing crisis to the 1987 and 2008 financial crises by looking at the evolution of the above-mentioned indicators when these crises arose.

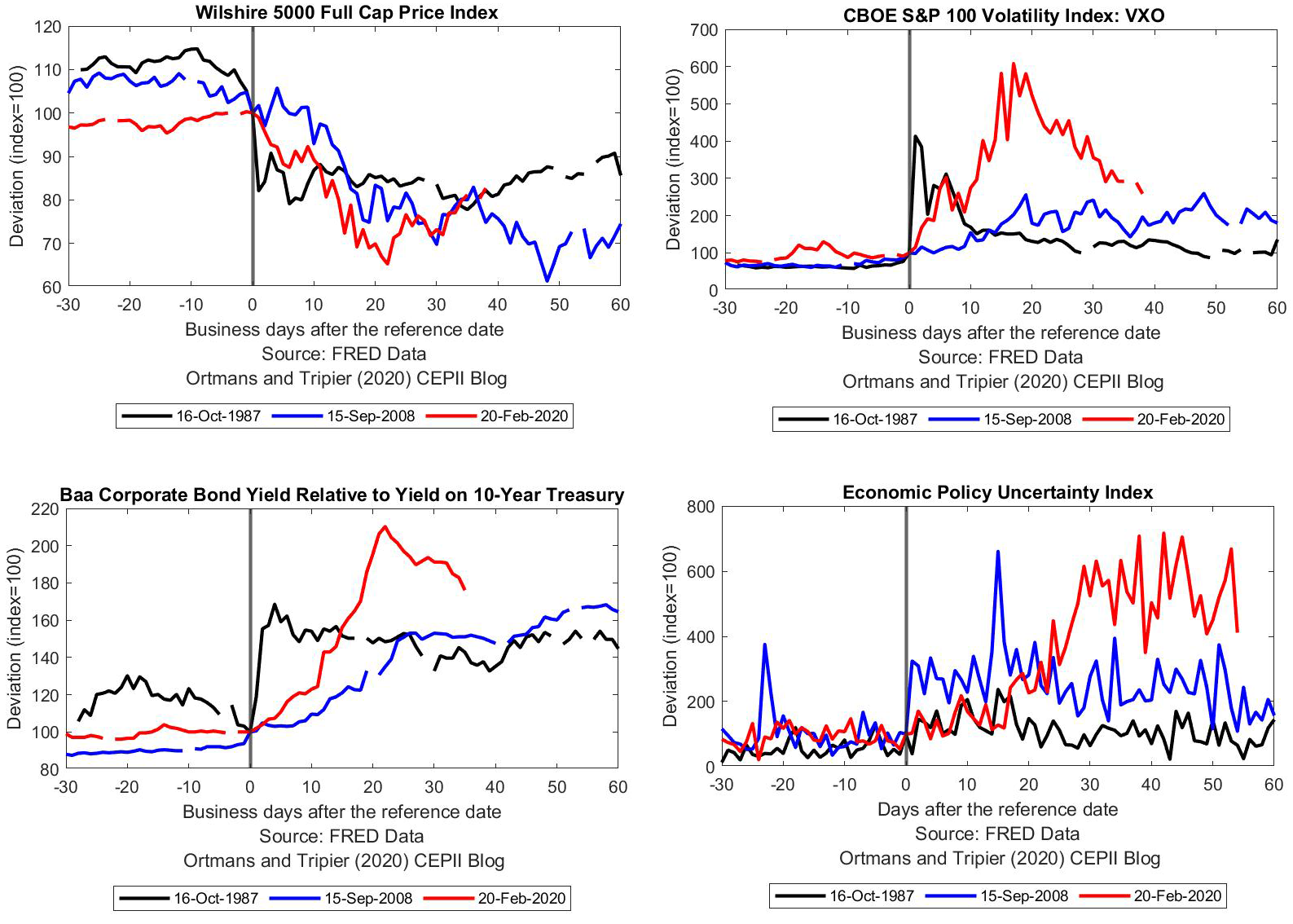

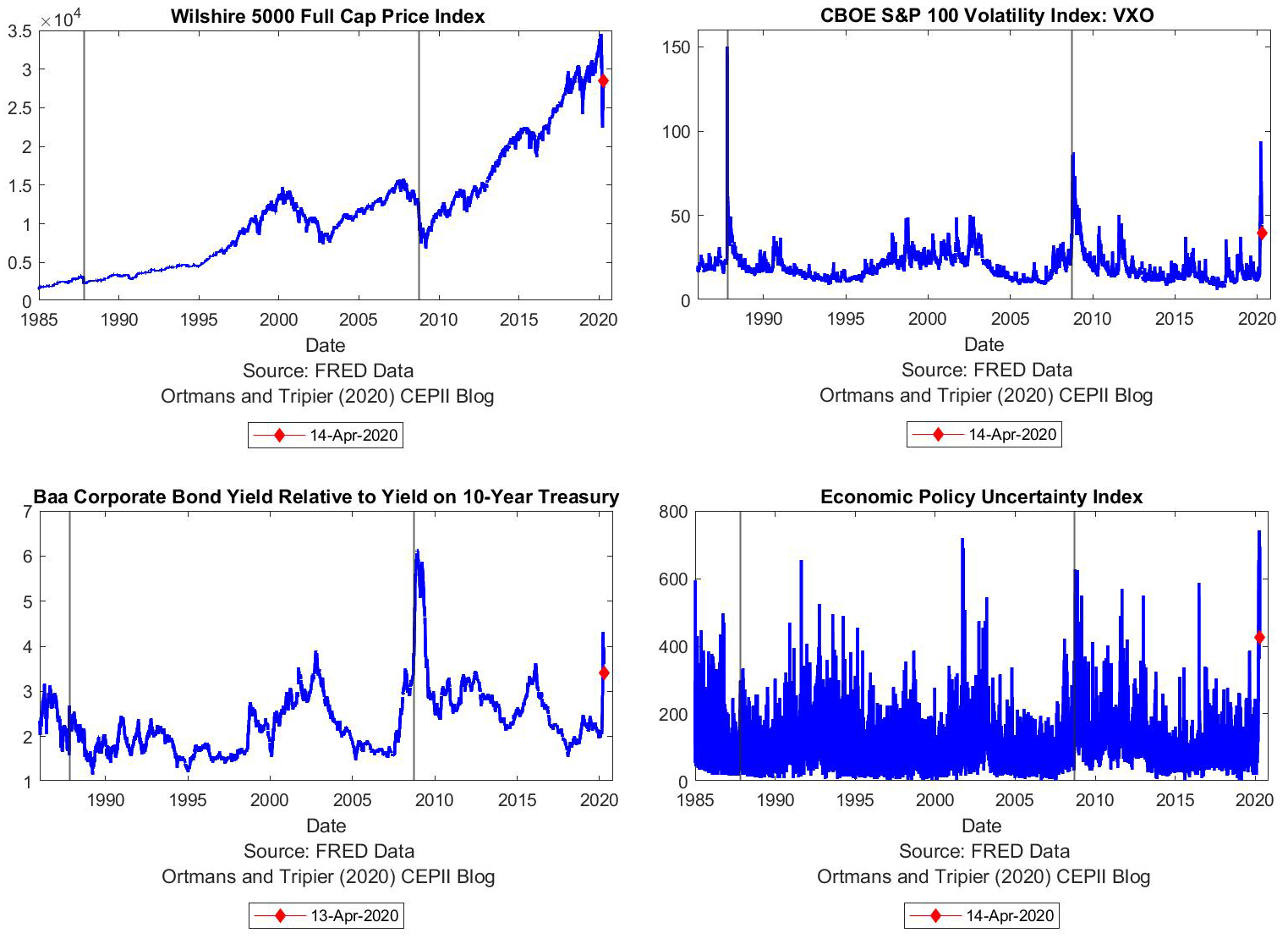

The dashboard tracks US uncertainty focusing on four daily indicators available on FRED.

- Stock market value index: the Wilshire 5000 index is a capitalization-weighted index of the market value of all US-stocks. A variation of this index can serve as an approximation of dollar changes in the U.S. equity market. A drop is usually interpreted as a decrease in the expected dividends by investors.

- Stock market fear index : the VXO provided by CBOE is a measure of constant 30-day expected volatility of the U.S. stock market. A rise of the VXO is usually interpreted as an increase in fear on the US stock market.

- Corporate defaut risk: the Moody’s Seasoned Baa Corporate Bond Yield Relative to Yield on 10-Year Treasury Constant Maturity is a measure of the default risk for U.S. corporates. A rise of the credit spread is usually interpreted as an increase in the risk of default on corporates debt.

- Political uncertainty: the economic policy uncertainty index measures policy-related economic uncertainty based on the newspaper coverage of policy-related economic uncertainty, the number of federal tax code provisions set to expire in future years, and the disagreement among economic forecasters.

Compared to these two crises, the Covid-19 crisis generates far more uncertainty.

- The stock market value index first plummeted by more than 30%, a downturn larger than in 1987 and 2008, before reaching the path observed in 2008.

- Stock market volatility has peaked at a level almost 6 times higher than that observed on February 20, 2020[3], before decreasing. However, this level still overshoots that observed at the beginning of the Covid-19 crisis, and is higher than in 1987 and 2008.

- Credit spread has more than doubled, before decreasing and staying at a high level over the Covid-19 crisis period (higher than in 1987 and 2008). This indicator highlights how the current crisis threatens the real economy.

- The increase in economic policy uncertainty overshot those observed during the last two financial crises.

The dashboard will be frequently updated as long as the Covid-19 crisis is ongoing.

[1] "There are very large uncertainties around the transmission of this virus, the likely effectiveness of different policies and the extent to which the population spontaneously adopts risk reducing behaviours. This means it is difficult to be definitive about the likely initial duration of measures which will be required, except that it will be several months." Imperial College Covid-19 Response Team March 16, 2020.

[2] "It’s very hard to say how big the effects will be or how long they will last. That’s going to depend of course on how widely the virus spreads, which is something that is highly uncertain and I would say, in fact, unknowable." Jerome Powell, press conference March 16, 2020.

[3] The reference date for the Covid-19 crisis, February 20th 2020, is based on visual inspection of Google Trend queries on "coronavirus" and coincides with the date of the publication of the Situation report - 31 by the WHO.

Aymeric Ortmans is a PhD student at Université Paris-Saclay (EPEE).

< Back