.png)

The exit from the U.S. zero interest-rate policy should be done gradually

Once again, the Federal Reserve has postponed the date of exit from the zero lower bound. We show that the pace of the tightening cycle matters more than the exact timing of the first interest rate hike for the macroeconomy.

By Stéphane Lhuissier, Fabien Tripier

On September 17, 2015, the Federal Open Market Committee (FOMC) decided to maintain its federal funds rate at its historically low level, i.e. a target range between 0 and 25 basis points, thereby keeping the most accommodative monetary policy stance implemented since the end of 2008.

However, Janet Yellen, Chair of the Committee, reminded us that most members of the FOMC still believed that « economic conditions [would] make it appropriate to raise the target range for the federal funds rate later this year ». We view this statement as keeping the door to a rate hike sooner rather than later. In this piece, we argue that at the current juncture, what matters most is not the timing but rather the pace at which the FOMC will design its tightening cycle. Our view concurs with Yellen’s, who considers that the initial rise in the target is far less important than the entire expected path of interest rates:

However, Janet Yellen, Chair of the Committee, reminded us that most members of the FOMC still believed that « economic conditions [would] make it appropriate to raise the target range for the federal funds rate later this year ». We view this statement as keeping the door to a rate hike sooner rather than later. In this piece, we argue that at the current juncture, what matters most is not the timing but rather the pace at which the FOMC will design its tightening cycle. Our view concurs with Yellen’s, who considers that the initial rise in the target is far less important than the entire expected path of interest rates:

« Let me again emphasize that the specific timing of the initial increase in the target range for the federal funds rate is far less important for the economy than the entire expected path of interest rates. »

Transcript of Chair Yellen’s FOMC Press Conference Opening Statement, September 17, 2015.

Transcript of Chair Yellen’s FOMC Press Conference Opening Statement, September 17, 2015.

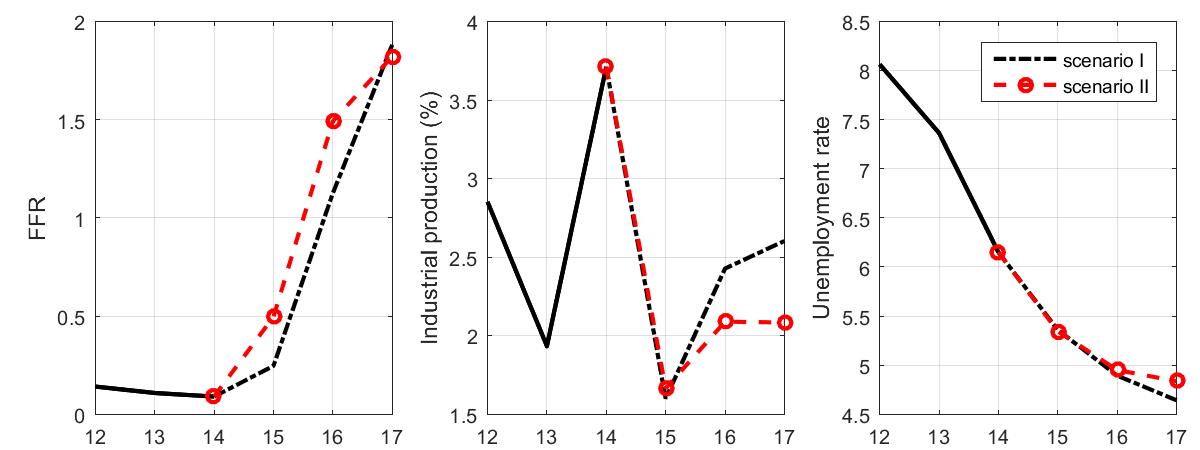

To illustrate how the steepness of the interest rate path matters for the economy, we employ a statistical forecasting model for the U.S. economy using market expectations as an input[1]. More specifically, we use the responses to survey of primary dealers conducted by the Federal Reserve of New York as a real life proxy the expected path of the policy rate of U.S. monetary policy. In our benchmark scenario, which corresponds to average expectations of primary dealers as of mid-2015, the target for the federal funds rate will evolve as follows for the next six quarters: 0.25% (Q1), 0.50% (Q2), 0.75% (Q3), 1.00% (Q4); 1.13% (Q5) and 1.63% (Q6). In this reference scenario (Figure 1), the pace of economic activity is expected to accelerate over the coming quarters, resulting in annual growth rates of industrial production that are higher in 2016 (2.4%) and 2017 (2.6%) than in 2015 (1.6%). Similarly, the unemployment rate should keep decreasing to below 5% in 2016. According to this benchmark scenario, a gradual exit from the Fed’s zero interest rate policy is not an impediment to a steady recovery of economic activity.

Figure 1: A gradual tightening cycle is supportive of economic activity

Figure 1: A gradual tightening cycle is supportive of economic activity

NB :Series are expressed in annual growth rates.

A more gradualist Fed would benefit the economy. To assess the effect of a faster exit from the zero interest rate policy, we simulate a second scenario. In it, the Federal Reserve announces that the federal funds rate will instead be systematically 50 basis points higher than those expected in the benchmark above, following a quarterly path of 0.75%, 1%, 1.25% and 1.5%. As shown in Figure 1, the announcement that monetary policy will be more contractionary than expected leads to a notable slowdown in economic activity. Under this alternative scenario, economic activity slows down (the growth of industrial production slows down by about 0.35% in 2016 and 0.50% in 2017). Likewise, unemployment becomes more sticky.

Overall, our results show that although the exit from the zero interest rate policy is already expected, the “steepness” of interest rate rises by the Federal Reserve has a first order impact on economic activity. Given the current degree of uncertainty surrounding the robustness of the US economic environment – in particular price and wage developments – we would argue that the Fed should err on the side of caution and opt for a gradual exit.

[1] The model is based on the methodology of Waggoner et Zha (1999) « Conditional forecasts in dynamic multivariate models », Review of Economics and Statistics, 81(4), 639-651, see CEPII Working Paper : Cheysson, Lhuissier and Tripier « Financial Factors in Baysian Structural VAR Models » forthcoming.

< Back